Why Standalone Financial Services Are Failing Gig Platforms (And What Actually Works)

Why Standalone Financial Services Are Failing Gig Platforms (And What Actually Works)

The gig economy is worth over $400 billion globally, but most platforms are still treating financial services like a side quest. They build their core marketplace, launch with basic payments, then later bolt on financial features as separate products. The result? Fragmented user experiences, operational nightmares, and missed retention opportunities.

After working across 19 different gigs and now building financial infrastructure for platforms, I've seen this pattern play out countless times. The platforms that thrive don't add financial services—they embed them from day one.

The Bolt-On Finance Trap

Here's how most gig platforms approach financial services:

- Phase 1: Launch with basic card processing (usually Stripe)

- Phase 2: Add instant payouts as a separate feature

- Phase 3: Partner with third-party providers for lending, insurance, tax services

- Phase 4: Struggle with integration complexity and user adoption

This approach fails because it treats financial services as products rather than infrastructure. The numbers tell the story:

- 67% of gig workers abandon platforms within 6 months due to payment friction

- Platform integration projects with standalone fintech providers average 8-12 months

- User adoption rates for bolt-on financial features rarely exceed 15%

The problem isn't the individual services—it's the approach.

Why Integration Hell Is Inevitable

When you bolt financial services onto an existing platform, you're essentially building three separate systems that need to talk to each other:

1. Core Platform Logic

Your marketplace handles job matching, user management, and core workflows. This system knows who your workers are, what work they're doing, and when they should get paid.

2. Payment Infrastructure

Usually Stripe or similar, handling card processing and basic payouts. This system knows about money movement but nothing about your business logic or worker relationships.

3. Additional Financial Services

Third-party providers for lending, early pay, insurance, tax services. Each has their own API, data requirements, and user experience patterns.

The result is what I call ""integration spaghetti""—dozens of API calls just to process a single payment, data inconsistencies across systems, and user journeys that feel bolted together because they are.

The Embedded Finance Alternative

Embedded finance flips this model. Instead of adding financial services to your platform, you build financial capabilities into your platform infrastructure from the ground up.

Here's what that looks like:

Single API, Complete Financial Stack

Rather than integrating with multiple providers, you connect to one embedded finance platform that handles:

- Payment processing and card intake

- Multi-party payment splits

- Instant settlement and payouts

- Onboarding and verification

- Tax handling and compliance

- Optional services (early pay, insurance, benefits)

Business Logic Integration

The financial infrastructure understands your platform's specific workflows:

- Healthcare platforms: Automated split payments between practitioners, facilities, and insurance

- Delivery platforms: Dynamic commission calculations based on distance, surge pricing, and tip handling

- Service marketplaces: Milestone-based payments with automatic escrow release

Unified User Experience

Workers interact with financial services through your platform's interface, not third-party apps. Everything from onboarding to tax documents lives within the experience they already know.

The MyGigsters Approach: Infrastructure Over Products

At MyGigsters, we've architected our platform around three core principles that make embedded finance actually work:

1. API-First Architecture

Every financial capability is exposed through clean APIs that integrate with your existing platform logic. Need to calculate commission splits based on custom business rules? That's a single API call, not a complex integration project.

2. Modular Implementation

Platforms can start with basic payment orchestration and add capabilities as they scale:

- Core Module: Payment processing, splits, instant payouts

- Compliance Module: Onboarding, verification, right-to-work checks

- Operations Module: Invoicing, tax handling, reconciliation

- Optional Modules: Early pay, insurance, super, tax advisory, perks

3. White-Label Experience

Workers never see MyGigsters branding. Every touchpoint—from onboarding forms to tax documents—carries your platform's brand and design language.

Real-World Impact: By The Numbers

Platforms using embedded finance infrastructure see dramatically different outcomes:

Implementation Speed:

- Standalone integrations: 8-12 months average

- Embedded finance: 2-4 weeks to go-live

User Adoption:

- Bolt-on financial features: 15% adoption rate

- Embedded financial capabilities: 85%+ adoption rate

Worker Retention:

- Platforms with embedded instant pay: 73% worker retention at 6 months

- Platforms with bolt-on instant pay: 31% retention

Operational Overhead:

- Multiple integrations: 40+ hours/week managing financial operations

- Single embedded platform: 5-8 hours/week

Implementation Framework: Getting It Right

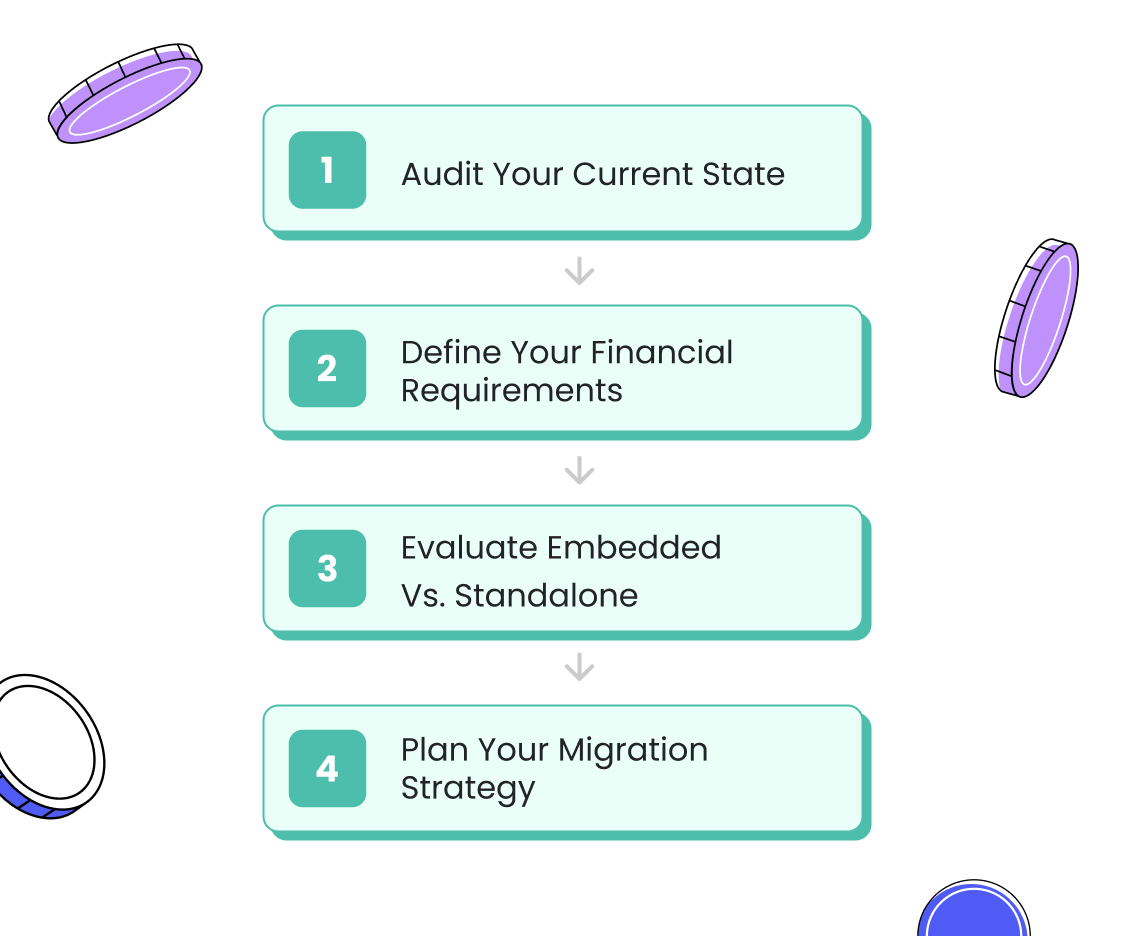

If you're building or rebuilding your platform's financial capabilities, here's a practical framework:

Step 1: Audit Your Current State

- Map your payment flows: Document every money movement in your platform

- Identify integration points: How many different financial APIs are you managing?

- Calculate hidden costs: Developer time, maintenance overhead, compliance burden

- Measure user friction: Where do workers drop off in financial workflows?

Step 2: Define Your Financial Requirements

- Core payments: What payment types do you need? (splits, instant, recurring)

- Compliance needs: What verification and onboarding requirements apply?

- Geographic scope: Domestic only or multi-currency/cross-border?

- Growth modules: What additional services will you need as you scale?

Step 3: Evaluate Embedded vs. Standalone

Use this decision tree:

- If you have fewer than 1,000 active workers → Start with Stripe + basic integrations

- If you have complex payment splits or compliance requirements → Go embedded from day one

- If you're planning multiple financial services → Embedded finance is the only scalable path

- If you're rebuilding existing financial infrastructure → This is the perfect time to embed

Step 4: Plan Your Migration Strategy

For platforms with existing financial integrations:

- Phase 1: Migrate core payment processing (lowest risk, highest impact)

- Phase 2: Consolidate compliance and onboarding

- Phase 3: Add new financial services through embedded platform

- Phase 4: Sunset legacy integrations

The Competitive Advantage

Platforms with properly embedded financial infrastructure don't just save operational overhead—they create sustainable competitive advantages:

Faster Feature Development: Need to add a new financial service? Deploy it through your existing embedded platform in days, not months.

Better Unit Economics: Embedded platforms typically offer better economics than assembling multiple point solutions.

Superior Analytics: All financial data flows through your platform, giving you complete visibility into worker behavior and business performance.

Reduced Compliance Risk: Single compliance framework covers all financial services, rather than managing multiple regulatory relationships.

Common Implementation Pitfalls

After helping dozens of platforms transition to embedded finance, these are the mistakes that kill projects:

1. Treating It Like a Traditional Integration

Embedded finance requires rethinking your platform architecture, not just adding new API calls.

2. Underestimating Data Migration

Moving worker payment histories and compliance records is complex. Plan 2-3x longer than you think.

3. Ignoring Change Management

Your operations team will need to learn new workflows. Factor in training and transition time.

4. Going All-In Too Fast

Start with core payment orchestration before adding advanced financial services. Get the foundation right first.

Looking Forward: The Infrastructure Advantage

The gig economy is maturing. The platforms that will dominate the next decade won't be those with the best job matching algorithms or the slickest mobile apps—they'll be the ones with the most seamless financial infrastructure.

Workers increasingly expect instant payments, transparent fees, integrated tax handling, and financial wellness tools. These aren't nice-to-have features anymore; they're table stakes for worker retention.

The question isn't whether to embed financial services—it's whether to build that infrastructure now or spend the next two years managing integration complexity while your competitors pull ahead.

Take Action: Start With The Foundation

If you're running a gig platform and recognizing these patterns, the path forward is clear:

- Audit your current financial stack using the framework above

- Calculate the true cost of your existing integrations (developer time + maintenance + opportunity cost)

- Model the impact of improved worker retention through better financial UX

- Plan your embedded finance strategy before your next major product development cycle

The platforms winning in 2026 embedded their financial infrastructure years ago. The question is: will you be ready for what comes next?

Ready to explore embedded finance for your platform? Book a demo with MyGigsters to see how payment orchestration, onboarding automation, and financial operations can be embedded into your existing workflow in 2-4 weeks, not months.

Frequently Asked Questions

Q: How long does it typically take to implement embedded finance infrastructure? A: With a proper embedded finance platform, most implementations take 2-4 weeks from integration to go-live. This includes payment processing, worker onboarding, and basic financial operations. Compare this to 8-12 months for assembling standalone solutions.

Q: What's the difference between embedded finance and traditional payment processing? A: Traditional payment processing handles money movement. Embedded finance integrates financial capabilities directly into your platform's business logic—understanding your workflows, user relationships, and compliance requirements. It's infrastructure, not just a service.

Q: Can existing platforms migrate to embedded finance without rebuilding everything? A: Yes, most embedded finance platforms are designed for migration. The typical approach is to start with payment processing, then gradually move compliance and additional services. Your existing user data and workflows remain intact.

Q: How does embedded finance improve worker retention? A: By removing friction from financial workflows—instant onboarding, seamless payments, integrated tax handling, and unified user experience. Platforms with embedded finance see 70%+ worker retention at 6 months versus 30-40% for bolt-on solutions.

Q: What compliance requirements does embedded finance handle? A: Embedded finance platforms typically handle payment compliance (PCI DSS), worker verification (identity, right to work, credentials), tax compliance (ABN/ACN checks, tax forms), and financial services licensing. This removes the compliance burden from your platform.

Q: Is embedded finance cost-effective for smaller platforms? A: For platforms with under 1,000 active workers, basic Stripe integration may be more cost-effective initially. But if you're planning financial services beyond basic payments, embedded finance typically offers better unit economics even at smaller scale."